|

|

|

|

|

Name

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

Are Wall Street Analysts Predicting Super Micro Computer Stock Will Climb or Sink?/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

San Jose, California-based Super Micro Computer, Inc. (SMCI) develops and manufactures advanced server and storage solutions built on a modular and open architecture. Valued at $33.8 billion by market cap, the company offers servers, storage systems, motherboards, full racks, chassis, and accessories worldwide. Shares of this AI server giant have underperformed the broader market over the past year. SMCI has declined 6.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 18.4%. However, in 2025, SMCI stock is up 91%, surpassing SPX’s 7.6% rise on a YTD basis. Narrowing the focus, SMCI’s underperformance is also apparent compared to the Technology Select Sector SPDR Fund (XLK). The exchange-traded fund has gained about 28.1% over the past year. However, SMCI’s robust gains on a YTD basis outshine the ETF’s 12.8% returns over the same time frame.

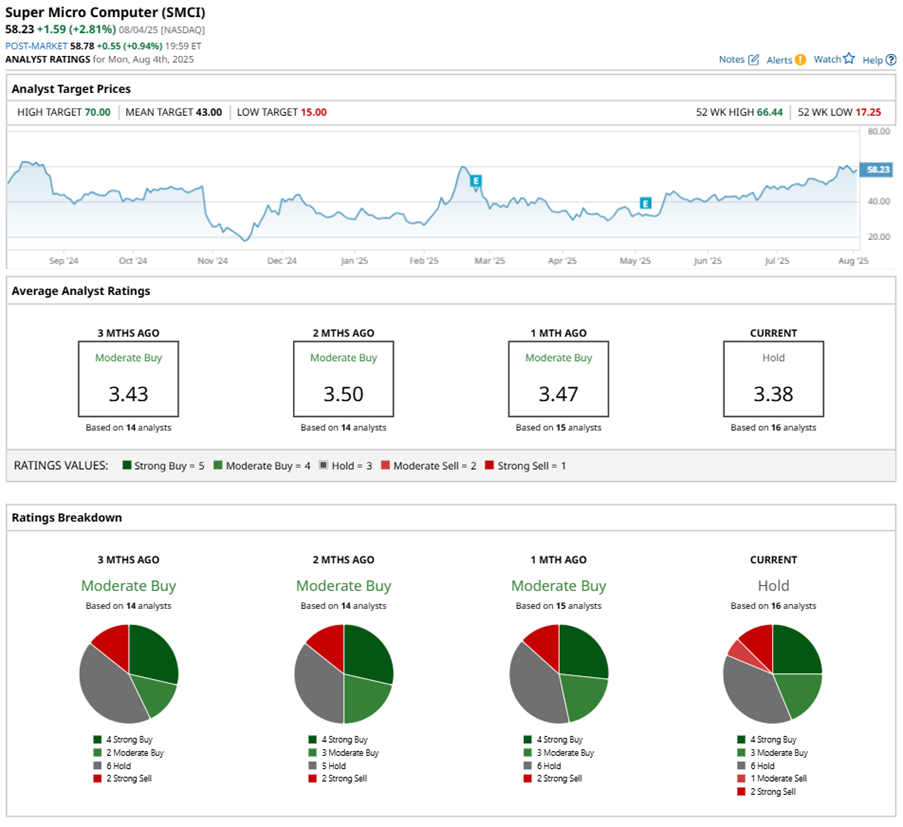

SMCI has been underperforming due to tariffs and delayed customer-platform decisions. The company is facing challenges, including customers evaluating next-generation AI platforms and experiencing margin contraction due to price competition. SMCI also had a one-time inventory write-down on older-generation components. Competition from Hewlett Packard Enterprise Company (HPE) and Dell Technologies Inc. (DELL) in the infrastructure-as-a-service space adds further pressure on SMCI. On May 6, SMCI shares closed up more than 2% after the company reported its Q3 results. Its adjusted EPS declined 53% year over year to $0.31. The company’s revenue totaled $4.6 billion, representing a 19.5% year-over-year increase. SMCI expects full-year revenue in the range of $21.8 billion to $22.6 billion. For the current fiscal year, ended in June, analysts expect SMCI’s EPS to decline 14.4% to $1.72 on a diluted basis. The company’s earnings surprise history is disappointing. It missed the consensus estimates in two of the last three quarters while beating the forecast on another occasion. Among the 16 analysts covering SMCI stock, the consensus is a “Hold.” That’s based on four “Strong Buy” ratings, three “Moderate Buys,” six “Holds,” one recommends a “Moderate Sell,” and two advocate a “Strong Sell.”

This configuration is less bearish than a month ago, with no analyst suggesting a “Moderate Sell.” On Jul. 31, Samik Chatterjee from JPMorgan Chase & Co. (JPM) maintained a “Hold” rating on SMCI with a price target of $46. While SMCI currently trades above its mean price target of $43, the Street-high price target of $70 suggests a 20.2% upside potential. On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |

|

|